Car Insurance Made Easy: Get Better Coverage Today

Car Insurance Made Easy , it’s not just a catchy slogan, but a real goal you can achieve. In this comprehensive guide, we break down the complexities of auto insurance into simple terms so you can get better coverage today. From finding car insurance quotes online to unlocking discounts and choosing the right policy, we’ve got you covered. Car Insurance Made Easy means understanding your options, saving money, and gaining peace of mind on the road.

Understanding Car Insurance Coverage Options

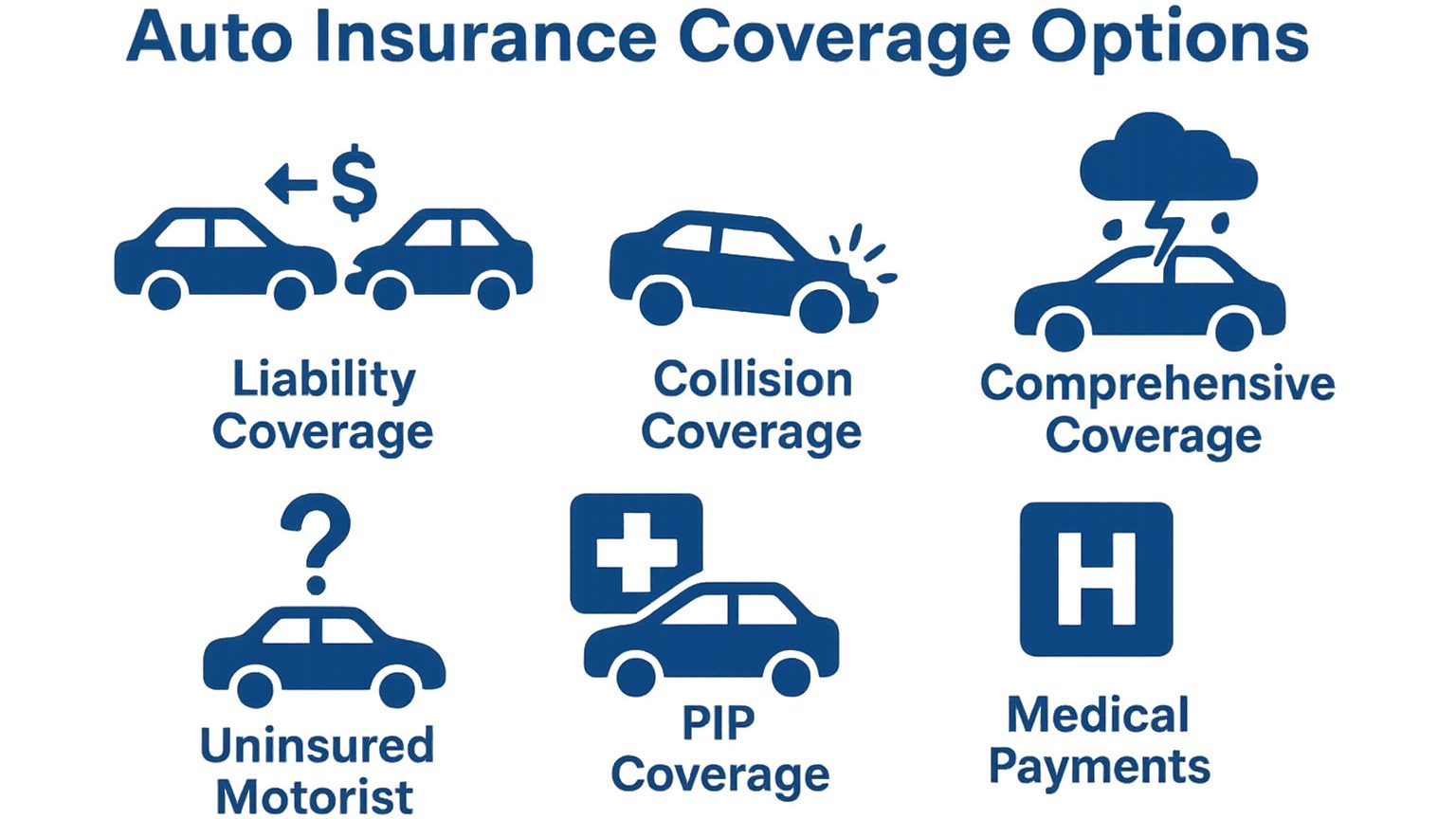

Illustration: A concept of car insurance protection, with hands shielding a car. Car insurance coverage options might seem confusing at first, but understanding them is key to making smart choices. Most policies include multiple types of coverage that protect you in different situations. Here are the main coverage options explained:

- Liability Insurance: Mandatory in nearly all states, liability coverage pays for injuries and property damage you cause to others in an . It’s the foundation of every auto policy and required by law to ensure victims are compensated.

- Collision Coverage: This pays for damage to your own car from a collision . If you crash into another vehicle or object, collision coverage helps repair or replace your car. It’s often required by lenders if you finance or lease your vehicle.

- Comprehensive Coverage: Comprehensive covers your car for non collision incidents , theft, vandalism, fire, natural disasters, falling objects, or animal strikes. Together with collision, it forms “full coverage” which gives broader protection for your vehicle.

- Uninsured/Underinsured Motorist (UM/UIM): UM/UIM coverage protects you if you’re hit by a driver with little or no insurance. About half of U.S. states require some form of UM/UIM because it helps pay for your injuries and damage when the at fault driver can’t.

- Personal Injury Protection (PIP) / Medical Payments: PIP required in no fault states or MedPay covers medical expenses for you and your passengers after an accident, no matter who was at . PIP can also cover lost wages and other related costs, and is mandatory in some states with no fault insurance systems.

Understanding these coverage types makes car insurance made easy, because you’ll know exactly what protection you have. Aim to carry enough liability coverage to meet state requirements and then some for better protection, and consider collision and comprehensive for your own car if it has significant value. The right combination of coverage options ensures you won’t be left with huge bills after an accident.

Comparing Car Insurance Quotes Online to Find the Best Rates

Shopping for insurance can actually be quick and convenient. By comparing car insurance quotes online, you can pinpoint the best deal for the coverage you need. Here’s how to make car insurance comparison simple:

- Gather Your Information: Before you start, have your driver’s license, vehicle details, and driving history handy. You’ll also need your current coverage limits if you have a policy, so you can compare “apples to apples.”

- Use Online Quote Tools: Many insurers and comparison websites let you get car insurance quotes online in minutes by entering your info. Take advantage of these free tools – the more quotes you get, the better your chances of finding a lower premium. In fact, experts recommend comparing quotes from at least 3–5 .

- Compare Coverage and Rates: Don’t just look at the price – examine the coverage each quote includes. A cheap quote might offer lower liability limits or higher deductibles. The goal is better coverage at a competitive rate, not just the lowest price. Check that each quote meets your needs and car insurance requirements .

- Look at Reviews and Reputation: Price is important, but so is service. Research each insurer’s customer satisfaction and car insurance reviews. An insurer with slightly higher rates might be worth it if they have superior claims service and reviews. Remember, the cheapest policy isn’t a bargain if the company fails you at claim time. Good service and claims handling are top reasons customers stay .

Car Insurance Made Easy tip: Do your online comparison when your current policy is up for renewal. Rates can change frequently, and another insurer might offer you a better deal now. According to recent data, auto insurance costs have been rising, so shopping around is more important than . With a few clicks, you can potentially save hundreds on your annual car insurance rates while keeping the same or better coverage.

Car Insurance for New Drivers

Being a new or young driver can feel expensive – and it’s true, car insurance for new drivers typically costs more due to limited experience. In fact, teen drivers can pay nearly four times more than older adults for the same . A 16 year old’s full coverage premium averages around $9,825 per year, which gradually drops to about $2,970 by age 25 as they gain . Don’t be discouraged! There are ways to make car insurance more affordable and easy for new drivers:

- Join a Parent’s Policy: If you’re a teen or student, getting added to a parent or guardian’s policy is often cheaper than buying your own. Families can take advantage of multi car discounts and spread the risk, which insurers reward with lower rates for young drivers.

- Good Student Discounts: Are you a student with good grades? Many insurers offer discounts often 5–15% for maintaining a “B” average or . This reward for responsibility can significantly cut costs for high school or college drivers.

- Driver Education and Training: Completing a driver’s education course or a defensive driving class can not only make you a safer driver but also qualify you for discounts. Some companies specifically offer a discount for young drivers who have taken approved safety courses.

- Choose the Right Car: The type of car you drive affects your premium. New drivers should consider a safe, moderate vehicle – one with good safety ratings and not too expensive to repair. Sporty cars or high horsepower engines tend to cost much more to insure, especially for teens.

- Consider Telematics Programs: Many insurers have usage based insurance programs like plug in devices or smartphone apps that monitor your driving. If you drive safely, you could earn sizable discounts. Safe driver programs can save participants up to 30% or more .This can be great for tech savvy young drivers willing to prove themselves with good driving habits.

With these strategies, even inexperienced drivers can get car insurance made easy and more affordable. Most importantly, focus on driving safely. As you build a clean driving record over time, your rates will gradually decrease. By age 25, insurers see you as a lower risk and your costs should drop a rewarding milestone for keeping safe on the road.

Car Insurance for Seniors

Car insurance isn’t just a concern for the young – older drivers need to manage premiums too. Car insurance for seniors can sometimes become pricier as age increases, because insurers worry about slower reflexes or health conditions. After about age 65–70, you might notice your rates creeping up. For example, the average annual premium for a 75 year old driver is around $2,620, which is a bit higher than the ~$2,358 paid by a 50 year old . The good news is there are ways seniors can keep insurance easy and affordable:

- Senior Discounts & Mature Driver Courses: Many insurance companies offer special senior or “mature driver” discounts. Taking a defensive driving course in your retirement years can not only refresh your skills but also earn you a discount with certain insurers. It’s a win win: safer driving and savings .

- Evaluate Your Coverage Needs: Seniors often drive fewer miles e.g., no daily commute. If you’ve significantly reduced your driving, ask your insurer about low mileage discounts or consider usage based insurance devices that charge based on miles driven. Less time on the road can mean lower risk and lower rates.

- Car Selection and Coverage Adjustments: If you’re driving an older vehicle that’s fully paid off, you might consider whether you still need comprehensive and collision coverage. Dropping these optional coverages can save money, but be sure you could afford to repair or replace the car out of pocket if an accident happened. Always keep at least the state required liability .

- Compare and Bundle Policies: Just as with any driver, seniors should compare quotes periodically. Some insurers are more “senior friendly” in their pricing. Also, if you own a home or have other insurance policies, bundling them e.g., home and auto with the same company can yield multi policy discounts. Bundling home and auto insurance can save around 7% on your car premium on a handy saving for those on fixed incomes.

Above all, car insurance made easy for seniors means not letting your policy renew each year without a second look. Circumstances change , maybe you now drive only twice a week, or perhaps there’s a new insurer in the market with better rates for your age group. Stay proactive, take advantage of any senior perks, and keep driving safely. Safe, experienced drivers in their golden years can still enjoy reasonable premiums by leveraging these tips.

Unlocking Car Insurance Discounts and Savings

Everyone loves a discount! Car insurance discounts are one of the best ways to reduce your premium and get better coverage for less money. Most insurers offer a variety of discounts , some you might know about, and some that might surprise you. Here are popular discount opportunities to look for:

- Safe Driver Discount: If you have a clean driving record no recent accidents or tickets, your insurer may reward you with lower rates. Additionally, enrolling in a telematics program like Progressive’s Snapshot or State Farm’s Drive Safe & Save can personalize your rate. Safe drivers in these programs can save up to 30% off and sometimes even more for the very best drivers.

- Multi Policy Discount: Combining policies with the same insurer for example, auto and homeowners insurance usually earns a discount on one or both policies. Bundling home and car insurance often saves around 5–10%; one analysis showed roughly 7% average savings on auto when you bundle . It’s convenient to have all your coverage in one place, and it costs less, too.

- Multi Car Discount: Insuring more than one vehicle on the same auto policy can reduce your rate per car. If your household has two or more cars, keep them on one policy. Many insurers knock about 10–25% off for multi car. Progressive, for instance, notes an average 12% savings for multi car .

- Good Student & Young Driver Discounts: As mentioned earlier, students with good grades or young drivers who take driving courses can get percentage discounts on their premiums. Every bit helps when rates for young drivers are high. Encourage the young drivers in your family to keep those grades up, it can directly translate into dollars saved.

- Low Mileage Discount: Do you drive only occasionally or have a very short commute? Let your insurer know. Drivers who put fewer miles on their car each year are at lower risk for accidents, and many companies offer discounts for staying under certain mileage thresholds. Some even have pay per mile insurance plans if you barely drive at all.

- Vehicle Safety and Features: Modern cars equipped with safety features like anti lock brakes, airbags, anti theft systems, and advanced driver aids can earn you discounts too. These features reduce the chance of injuries or theft, so insurers may give a small break on premiums for having them.

- Other Discounts: There are many niche discounts out there. For example, you might get a discount for being a senior or a member of certain organizations . Going paperless or paying your full premium upfront can save a few more bucks. Even shopping for quotes online often gives a small discount , some insurers provide an “online quote” or “sign online” discount for buying your policy through their website without paper forms.

When shopping for a policy, always ask about available discounts , you might be surprised at what’s offered. A combination of several discounts together can significantly lower your car insurance rates. Car Insurance Made Easy is also about being a smart shopper: take a little time to double check that you’re getting every discount you qualify for. It can add up to substantial savings while you maintain the coverage you need.

Choosing the Right Car Insurance Policy

Finding the right policy isn’t just about the cheapest price it’s about choosing a car insurance policy that offers great coverage, reliable service, and fits your specific needs. You want an insurer that will be there for you when it counts during a claim or emergency and a policy that meets all legal and personal requirements. Here are some key considerations to make car insurance selection easy:

- Coverage vs. Cost: Figure out how much coverage you truly need. At minimum, you must meet your state’s car insurance requirements for liability . But minimums are often too low to fully protect your assets, so consider higher liability limits if you can afford it. If you have a newer or valuable car, full coverage is wise and if you have a loan or lease, it will be required by the lender. Balance getting as much coverage as makes sense for you, while using the comparison and discount tips above to keep it affordable.

- Deductible Decisions: Your collision and comprehensive coverage come with a deductible . A higher deductible e.g. $1,000 instead of $250 can lower your premium, but be sure you could comfortably pay that amount in an emergency. Adjusting deductibles is a personal choice to manage premium vs. potential expense.

Beyond coverage and cost, think about the insurer’s reputation and how the policy is delivered. Are you comfortable with a digital only company, or do you prefer an agent you can call? Is the claims process straightforward? These factors determine your experience as a customer.

Read Car Insurance Reviews and Ratings

One of the best ways to gauge an insurer’s quality is by checking car insurance reviews and third party ratings. Look up customer reviews for insight on others’ experiences with claims and customer service. Additionally, consult independent ratings and studies:

- J.D. Power and Consumer Reports: Each year, J.D. Power releases an Auto Insurance Satisfaction Study ranking major insurers by region. According to the 2025 study, overall customer satisfaction with auto insurers has room for improvement , over one third of customers surveyed are not very satisfied with their insurer’s . Notably, the study found that while a good price attracts customers, good service and a smooth claims experience are what keep them with an insurer over the long . This tells us that it’s worth considering service quality, not just price, when you choose a policy.

- Financial Strength Ratings: Check ratings from agencies like A.M. Best, Moody’s, or Standard & Poor’s for an insurer’s financial stability. A company with excellent financial strength is more likely to pay claims promptly and fully, even in widespread disaster situations.

- State Insurance Department and Complaint Index: Many state insurance departments publish complaint ratios for insurers basically how many complaints a company gets relative to its size. A low complaint index is a good sign. You can also see if an insurer has a history of consumer issues.

In short, do a little homework on your shortlist of insurers. An insurer that combines competitive rates with high ratings and positive reviews is ideal. Remember that car insurance made easy isn’t just about buying a policy quickly, it’s about confidently choosing a company that will deliver when you need help.

Understand Policy Details and Requirements

Before finalizing your policy, make sure you understand the fine print and that you meet any necessary car insurance requirements:

- State Legal Requirements: As mentioned, almost every state requires drivers to carry a minimum amount of liability . Some states also require other coverages like personal injury protection (PIP) or uninsured motorist coverage. Know what’s mandated in your state , for example, Florida uniquely requires PIP and property damage liability only, no bodily injury liability, whereas New Hampshire is the only state that doesn’t mandate car insurance . Failing to meet your state’s requirements can result in fines, license suspension, or worse, so double check that your new policy complies with local laws.

- Lender or Lease Requirements: If your car is financed or leased, your finance company will require you to have full coverage both collision and comprehensive and sometimes gap insurance. This protects their interest in the vehicle. Make sure any policy you choose satisfies the lender’s coverage limits and deductible requirements outlined in your loan or lease .

- Policy Terms and Exclusions: Read through your policy documents . Take note of your coverage limits, deductibles, and any exclusions. For example, standard policies usually won’t cover commercial use of your car or racing, etc. Knowing these details ahead of time prevents nasty surprises later. If something is unclear, ask your insurance agent or the company’s representative. Part of making insurance easy is asking questions now so you fully understand your protection.

- Update Your Policy as Life Changes: Ensure your policy stays up to date. Did you move to a new address or change where you park your car? Did your annual mileage drop because you retired or started working from home? Keep your insurer informed, as these factors can affect your rate or coverage needs. Also, if you make improvements like installing an anti theft device, let them know, it could earn a discount.

By reading reviews and understanding requirements, you’ll choose a policy that not only fits your budget, but also gives you confidence. The right car insurance policy is one that you know will protect you in an accident, meets all legal obligations, and comes from a dependable insurer. When you have that, you truly achieve Car Insurance Made Easy.

Summary Table: Car Insurance Made Easy

| Section | Key Points |

|---|---|

| What “Car Insurance Made Easy” Means | Simple understanding of coverage, comparing quotes, saving money, and choosing the right policy. |

| Main Coverage Options | • Liability (required in most states) • Collision (covers your car in accidents) • Comprehensive (covers theft, fire, etc.) • UM/UIM (protects you from uninsured drivers) • PIP/MedPay (medical coverage) |

| How to Compare Quotes Online | • Gather info • Use comparison sites • Review coverage, not just price • Check reviews and reputation • Re-check rates yearly |

| For New Drivers | • Join parent’s policy • Good student discounts • Choose safe cars • Use telematics apps • Drive safely to lower future rates |

| For Seniors | • Take mature-driver classes • Review coverage yearly • Use low-mileage discounts • Bundle policies • Compare “senior-friendly” insurers |

| Ways to Save Money (Discounts) | • Safe driver • Multi-policy (home + auto) • Multi-car • Good student • Low mileage • Safe vehicle features • Paperless/pay-in-full |

| Choosing the Right Policy | • Balance cost vs. coverage • Understand deductibles • Read reviews & ratings • Meet state requirements • Update policy after life changes |

| Final Takeaway | Review your policy yearly, compare smartly, use discounts, and choose coverage that protects you and your car. |

Final Thought

In conclusion, Car Insurance Made Easy is all about knowledge and smart choices. By learning about coverage options, comparing quotes online, and leveraging discounts, you’re empowering yourself to get better coverage today without overspending. Remember, car insurance is not a one and done deal, it’s wise to review your policy at least once a year, shop around, and adjust your coverage as your life changes. With the tips in this guide, you can approach your auto insurance with confidence instead of confusion.

References

- Insurance Information Institute (III): https://www.iii.org

- National Association of Insurance Commissioners (NAIC): https://www.naic.org

- J.D. Power Auto Insurance Study: https://www.jdpower.com

- Consumer Reports – Car Insurance Ratings

- DMV.org – State Insurance Requirements

FAQ for Car Insurance Made Easy

1. What factors affect my car insurance rates?

Insurance rates depend on your age, driving history, location, vehicle type, credit score, and coverage selections.

2. How often should I compare car insurance quotes?

Experts recommend comparing car insurance quotes online at least once a year or before each renewal.

3. Is minimum coverage enough?

Minimum coverage meets state laws, but often isn’t enough to fully protect you in a major accident. Higher limits are recommended.

4. How can new drivers reduce insurance costs?

Join a parent’s plan, maintain good grades, choose a safe car, and use telematics to prove safe driving.

5. Why do seniors pay more for car insurance?

Rates may rise due to increased accident risk, but seniors can still save by taking mature driver courses, bundling policies, and comparing rates yearly.